CSRD: Requirements and Implementation for Executives and CFOs in 2025

Early involvement of executives and CFOs as a key success factor in CSRD

A critical aspect of CSRD implementation in 2025 is the active involvement of senior management, as the requirements have a significant impact on corporate financial governance. The primary focus is to provide executives and CFOs with a constructive perspective on sustainability. This article outlines the key elements of the CSRD Regulations and their implementation, specifically addressing the needs of executives and CFOs.

Context and requirements of the CSRD guidelines

The Corporate Sustainability Reporting Directive (CSRD) integrates sustainability reporting into accounting law and affects numerous companies that were not previously subject to reporting requirements. A sustainability report must be prepared in accordance with the European Sustainability Reporting Standards (ESRS). While the CSRD provides the overarching framework, the ESRS outline the specific reporting requirements.

CSRD implementation

The CSRD addresses core topics that are highly relevant for both executives and CFOs. There are three key focus areas that affect all companies subject to reporting obligations:

Additionally, it is crucial to examine how these areas can be integrated into existing financial reporting processes. Sustainability reporting requirements pose significant challenges, particularly for small and medium-sized enterprises. Learn more about the steps, common barriers and proven best practices for successful implementation.

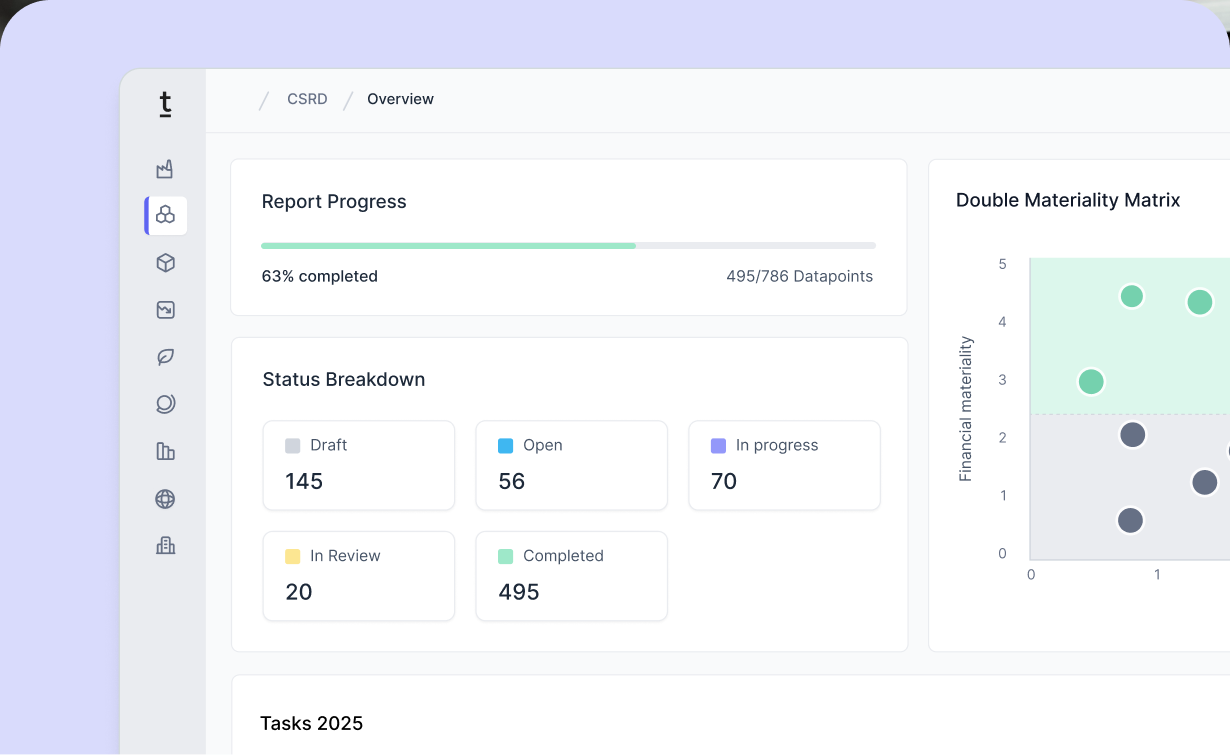

Double Materiality Assessment as the foundation of CSRD

The Double Materiality Assessment (DMA) is the basis of CSRD reporting, enabling companies to identify and evaluate topics that impact the organization and those affected by it. Early collaboration with auditors and effective stakeholder involvement are critical to successfully navigating the DMA.

Challenges in DMA

- Stakeholder consultation: Engaging stakeholders effectively requires diverse formats, such as online surveys, workshops, or IRO (Impacts, Risks, Opportunities) assessments.

- IRO definition: Identifying environmental and societal impacts demands a deep understanding of ESRS topics, including specific requirements like “substances of concern” or “substances of a particular concern.”

- IRO assessment: Assessing impacts using qualitative metrics such as "scale" and "scope" is challenging due to their subjective nature. Establishing appropriate thresholds also poses difficulties.

- DMA documentation: Preparing precise documentation for audit purposes is essential.

- Alignment with sustainability goals: Defining and aligning sustainability objectives with identified IROs must be ensured.

Best Practices for DMA

- Stakeholder consultation: It is important to thoroughly document stakeholder engagement to support audit readiness. You should focus as well on involving a manageable number of stakeholders with extensive ESG knowledge and familiarity with the company's operations to increase the reliability of input. In case direct engagement is impractical, representatives such as the sales team can act as proxies (e.g., for customer interests).

- IRO definition and assessment: IRO databases and external expertise can be used to define and evaluate IROs effectively. Align the assessment process, evaluation criteria, and documentation approach with auditors and involve senior management for verification and approval.

- Sustainability goals: Opt for relative benchmarks rather than absolute targets when defining sustainability objectives, as they offer greater flexibility and adaptability to your company’s unique circumstances.

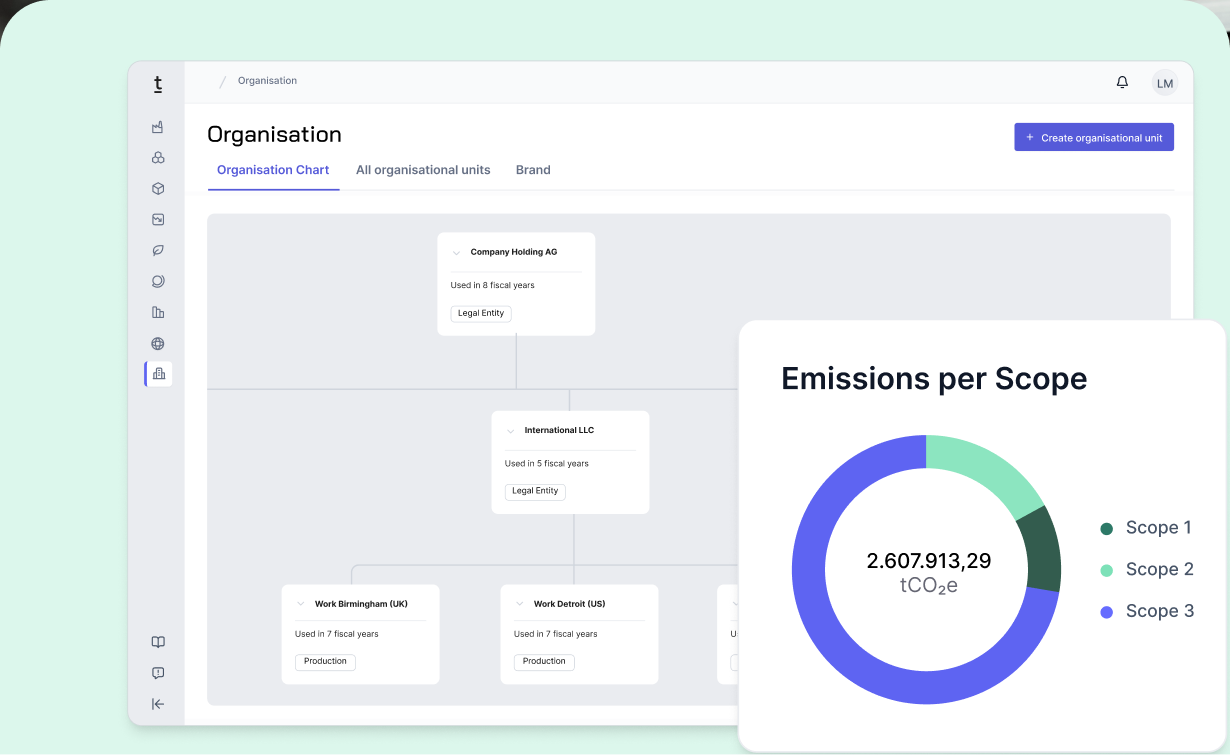

Corporate Carbon Footprint as part of the CSRD

The calculation of a Corporate Carbon Footprint (CCF), representing a company’s CO₂ Balance, requires extensive data collection across various areas of the organization. Coordinated process management is critical to success.

Companies are at different stages in their carbon accounting journey: while some are still in the orientation phase, others have already completed Scope 1, 2, and 3 assessments and defined decarbonization targets. Regardless of their progress, CCF is a fundamental component of any sustainability strategy. The key challenge for all organizations lies in identifying appropriate data sources and applying calculation methodologies that meet reporting obligations.

Challenges in CCF

- Scope 1 and 2: These baseline data are typically readily available, often derived from sources such as the Energy Efficiency Act or energy management systems like ISO 50001.

- Scope 3: The primary challenge lies in obtaining the necessary data. The key categories with the highest CO₂ emissions typically include procurement and the product use phase. However, data from suppliers is often sparse or unavailable. This issue extends to other categories as well, such as employee commuting.

- Technical capacity for data collection: Many companies lack sufficient IT systems for efficient data collection, leading to time-consuming and manual processes.

Best Practices for CCF

- Materiality assessment Scope 3: Identify emission hotspots, such as procurement and the product use phase, to prioritize efforts effectively.

- Calculation models and benchmarks for Scope 3: Collaborating with specialized consulting firms can help align methodologies and calculation models, making data estimation more manageable.

- Data collection for Scopes 1 to 3: Preparing for Scope 3 data collection well before the end of the fiscal year is crucial. Relevant data points and cost centers should be integrated into the financial accounting system. Comparing results with industry benchmarks, such as the Carbon Disclosure Project, can also help identify data gaps and best practices.

- Additionally, leveraging software-based CCF calculation tools, including sector-specific emissions factor databases and, if applicable, PCF calculation, provides a streamlined and scalable solution.

The role of the EU Taxonomy in the context of the CSRD

As part of the CSRD, compliance with the EU Taxonomy is required. This involves assessing economic activities based on their alignment with the EU’s environmental objectives. Conducting extensive analyses and preparing documentation in advance, ideally before the start of the fiscal year, is inevitable. Integrating these processes into accounting structures and ensuring early planning are key to efficient implementation.

Challenges in EU Taxonomy

- Complex Taxonomy assessments: Detailed knowledge of materials, technologies, and business operations is necessary to evaluate activities.

- Separate evaluation of activities: Economic activities related to revenue, investments, and operating expenses must be assessed individually per The Climate Delegated Act.

- Limited data availability: Identifying the required information for classification within the company can be difficult.

- Missing accounting structures: Relevant cost types are often not separately recorded in accounting systems.

Best Practices for EU Taxonomy

- Early planning: Identify taxonomy-eligible revenues, investments, and operating expenses before the fiscal year begins. This ensures their separate recording in accounts or cost centers.

- Comprehensive review: All economic activities should be assessed for taxonomy eligibility, such as leasing costs for company vehicles as potential operating expenses. Prioritizing activities with uncertain compliance criteria can be beneficial starting with the least clear criteria first may help avoid additional reviews.

- Creating clarity: Avoid double counting by using clear classifications. Additionally, take advantage of the relief measures available in the first year, such as omitting disclosures for prior years.

Early planning facilitates CSRD implementation

Proactive and structured engagement with the CSRD and its related requirements is the first step toward success. Close collaboration with executives, the finance department, and auditors is essential. Support through software tools or consulting can further streamline processes and significantly reduce the burden on companies.

How Tanso can support you with CSRD

Tanso provides a sustainability software specifically designed to meet the needs of manufacturing companies. It enables efficient, data-driven management through modules for corporate and product-level carbon accounting, as well as compliance with extensive ESG reporting obligations. With the highest data standards, automated processes, and seamless collaboration across departments and locations, Tanso helps companies save time, ensure compliance, and optimize synergies.

.avif)

.jpg)

.jpg)

-p-800.webp.avif)

-min-p-800.webp.avif)

-p-800.webp.avif)