EU Taxonomy: Implementation and connection with the CSRD

What is the EU Taxonomy?

The EU Taxonomy is a central element of the European Green Deal. This instrument provides a classification for the identification of sustainable economic activities. The aim is to promote targeted investment in environmentally friendly innovations in order to drive forward the green transition within the EU.

By supporting the EU's goals of climate neutrality by 2050 and a significant reduction in greenhouse gas emissions by 2030, the EU Taxonomy serves as a guideline for investors who wish to invest in sustainable projects.

According to the EU Taxonomy Regulation, an economic activity is classified as sustainable and therefore Taxonomy-compliant if it contributes substantially to at least one of the six defined environmental objectives without causing significant harm to other objectives (principle of “Do No Significant Harm” - DNSH). In addition, investments and activities must comply with basic social and human rights standards.

The focus is on the following six environmental objectives:

- Climate change mitigation

- Climate change adaptation

- Sustainable use and protection of water and marine resources

- Transition to a circular economy

- Pollution prevention and control

- Protection and restoration of biodiversity and ecosystems

EU Taxonomy Reporting: Framework and interfaces to CSRD

From 2025, all large companies that are subject to the requirements of the CSRD (Corporate Sustainability Reporting Directive) and therefore also the NFRD (Non-Financial Reporting Directive) will be obliged to report in accordance with the EU Taxonomy.

This obligation affects a broad range of companies in the EU and places new demands on transparency in sustainability reports: Taxonomy-compliant business activities must be disclosed within the management report and quantified according to their contribution to revenue, capital expenditure and operating expenses. The requirements of the CSRD are also published in the management report, albeit in separate sections.

In terms of data collection and preparation, the overlap between the CSRD and the EU Taxonomy is very limited. Within the CSRD, only the disclosure of Taxonomy-eligible activities in connection with fossil gas is requested, stating the respective sales revenues ESRS 2 SBM-1 40 (d)i.

The EU Taxonomy requirements relate to financial data from the annual financial statements. The greatest effort in the recurring implementation of the EU Taxonomy lies in the collection of key performance indicators and the monitoring of changes in the delegated act. Effective compliance with these guidelines is ensured by integrating them into existing reporting processes and systems. Implementation should therefore be carried out in close cooperation with the finance or controlling department.

-

Both the CSRD and the EU taxonomy are included in the management report. While the CSRD is based on non-financial data points, the EU taxonomy is based on financial performance indicators.

Both the CSRD and the EU taxonomy are included in the management report. While the CSRD is based on non-financial data points, the EU taxonomy is based on financial performance indicators.

Four steps to EU Taxonomy

The following steps provide an overview of the reporting process, which may vary depending on the company's specific situation. It is important to consider the current EU directives and legal requirements.

1. Preparation

Reporting on EU Taxonomy will require both time and extensive resources to prove eligibility and alignment to the level that auditors require to comply with the reporting regulations.

Establish a project team and plan

While controlling and finance are heavily involved, responsibility for EU Taxonomy reporting often rests with the sustainability team. Plan sufficient time to complete the four steps and submit your CSRD report on time, as alignment (step 3) often requires internal and external expertise, resources, and budgets. In the first year, anticipate additional work to understand the regulation and its application. Start the eligibility and alignment screening early to ensure timely reporting.

Identify your financial data structures and existing social safeguards

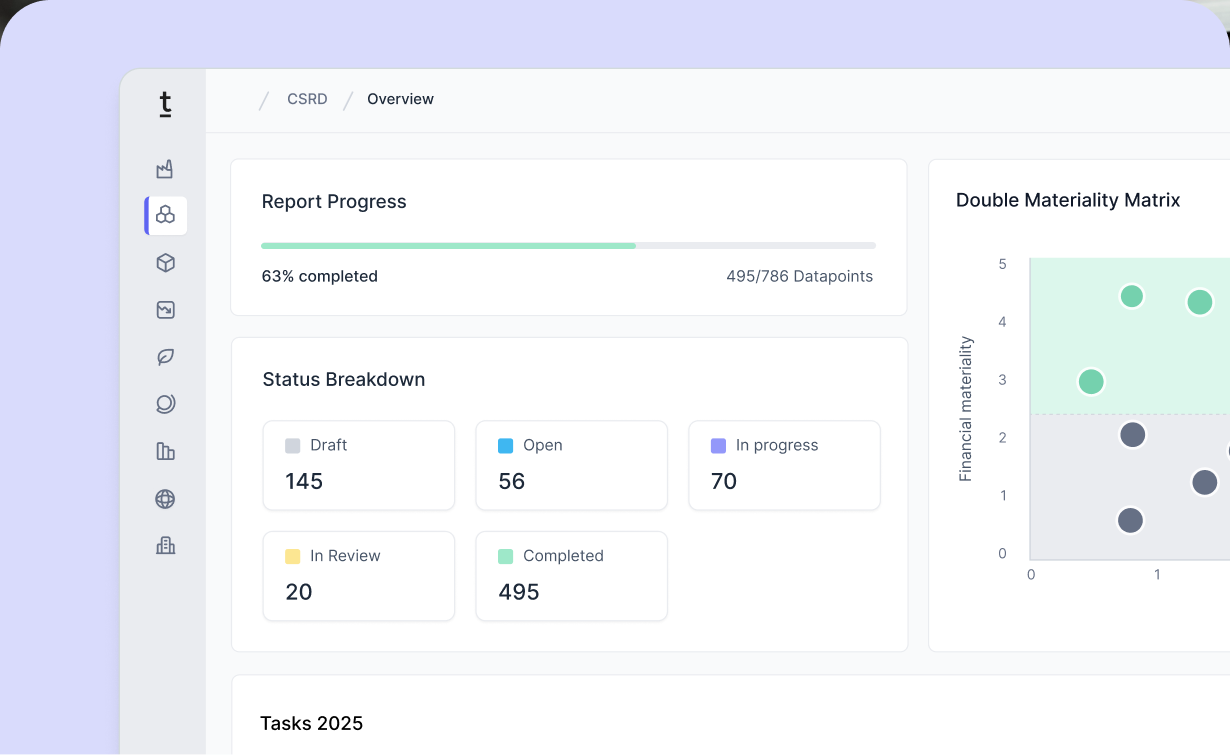

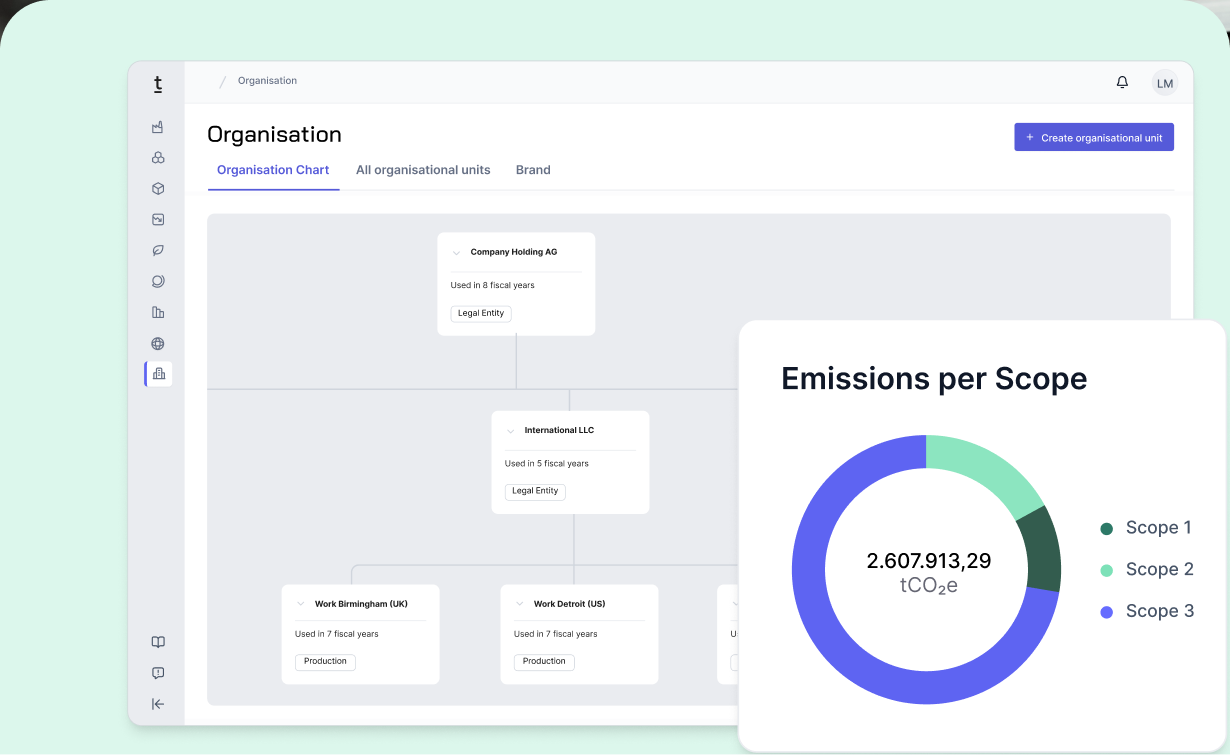

The EU Taxonomy classifies a company’s turnover, CapEx, and OpEx as non-eligible, eligible, or aligned, often shown in a donut chart. To classify activities effectively, you need to understand your financial data structures, such as accounts, cost centers, locations, or NACE codes. Also familiarize yourself with standards like ILO conventions, OECD guidelines, UN Guiding Principles, and the EU Charter of Fundamental Rights.

2. Eligibility

Identify the eligibility of the company’s activities

There are 148 eligible economic activities covering 198 unique NACE codes across 16 sectors. You can explore them on the EU Taxonomy Compass or in the Tanso app. Some activities are categorized as “Enabling” or “Transitional.” Enabling activities support others' substantial contributions, while transitional activities address the lack of low-carbon alternatives. For eligibility reporting under Article 10 of the Disclosures Delegated Act, these activities are treated like any others. Begin by identifying all economic activities in your company, including turnover, CapEx, and OpEx. Examine investment decisions and daily operational costs to classify them accurately.

Allocate turnover, CapEx & OpEx to eligible activities

After identifying potential EU-eligible activities, the next step is to match your company’s turnover, CapEx, and OpEx activities with the EU Taxonomy descriptions, which determine eligibility. For example, “Installation, maintenance and repair of renewable energy technologies” differs from “Electricity generation using solar photovoltaic technology.” This distinction is particularly important for CapEx classification (see wtep 4 -Reporting).

3. Alignment

The purpose of the EU Taxonomy is to facilitate the flow of investment towards projects that genuinely benefit the environment. By providing clear criteria, the Taxonomy aims to reduce market fragmentation and protect investors from greenwashing, thus enhancing the credibility of sustainable finance. This framework also encourages companies to transition to more sustainable practices, contributing to the EU's broader climate and sustainability goals.

Identify EU taxonomy alignment potential for your eligible activities

Start by reviewing the Technical Screening Criteria (TSC) for each eligible activity and its environmental objective in the EU Taxonomy. Some activities, like “Renovation of existing buildings,” can align with multiple objectives (e.g., Climate Mitigation, Climate Adaptation, Circular Economy). In such cases, allocate the activity to the most relevant objective and highlight it in bold in the final report to avoid double counting and ensure KPI consistency.

Derive & prioritize projects from Technical Screening Criteria (TSC)

Meeting TSC requirements can be extensive, requiring careful planning and resource allocation to prove alignment. The criteria mandate a substantial contribution to one objective and DNSH compliance for the other five. TSC are specific to each activity and detailed in the Delegated Acts Annex. First-time reporters should focus on proving and documenting existing alignment, often at the level of product lines, services, projects, or cost centers.

Prove substantial contribution for products, services and investments

Most companies seek external support—via consultancies, tools, or third-party verifiers—to prove EU Taxonomy alignment. Once the plan is in place, substantial contribution can be validated. Documentation may include Product Carbon Footprints (PCF), Energy Performance Certificates (EPC), third-party verification reports, or other evidence of compliance.

Prove DNSH for the remaining 5 objectives

Aligned activities must be reviewed for adverse effects on the other five environmental objectives. DNSH compliance ensures progress on one objective doesn’t come at the expense of others, highlighting interdependencies. Many criteria are tied to EU legislation or reference documents like Best Available Technologies (BAT). Objectives marked “N/A” in the TSC are not relevant for DNSH.

Implement and document minimum safeguards

Companies must implement and document due diligence and corrective measures to ensure compliance with OECD Guidelines, UN Guiding Principles, and ILO Core Standards. This includes detailing how human rights risks in operations, value chains, and business relationships are addressed, demonstrating adherence to the minimum safeguards in Article 18 of the EU Taxonomy.

4. Reporting

Define allocation models & quantify KPIs

To quantify Taxonomy eligibility and alignment, calculate the proportion of turnover, CapEx, and OpEx linked to Taxonomy-aligned activities (numerator) relative to their total amounts (denominator).

Turnover is net revenue as defined under IAS 1, paragraph 82(a). Revenue from activities contributing to Climate Adaptation is not eligible, as once an activity is climate-resilient, its turnover cannot count as eligible.

CapEx includes expenditures for assets or processes tied to Taxonomy-eligible activities:

- (a): Directly linked to eligible activities (e.g., building an energy-efficient office).

- (b): Part of plans to expand or enable alignment (e.g., investing in low-carbon production lines).

- (c): Related to outputs or measures enhancing efficiency and reducing emissions (e.g., solar panel installations).

OpEx includes direct, non-capitalized costs like R&D, renovations, short-term leases, maintenance, and servicing assets to ensure functionality. Excluded are overheads, raw materials, operating machinery, and utilities.

Publish EU Taxonomy disclosures in the annual sustainability statement

The EU Regulation requires companies to include EU Taxonomy information in the CSRD-based sustainability statement within the annual report, positioned near the environmental ESRS. This section typically includes the eligibility and alignment assessment and tables for turnover, CapEx, and OpEx.

The EU template contains both the results of the conformity assessment for each taxonomy-eligible activity and its expenditure according to one of the performance indicators.

-

Tanso is the complete solution for sustainability and non-financial KPIs. Would you like to find out how Tanso can help you set up an audit-proof standard process for CSRD reporting? Book a demo here.

.avif)

.jpg)

.jpg)

-p-800.webp.avif)

-min-p-800.webp.avif)

-p-800.webp.avif)