Gross vs. net assessment of IROs in CSRD & ESRS

What is the meaning of IROs within the CSRD?

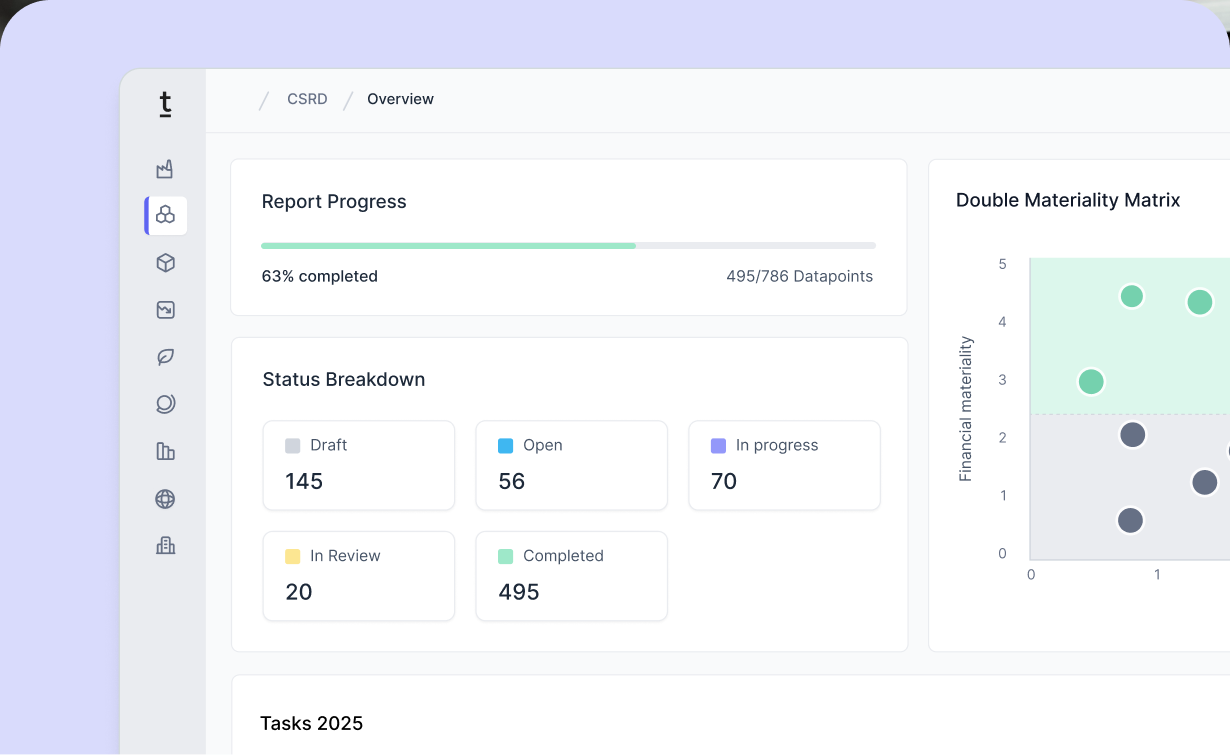

The CSRD begins with the Double Materiality Assessment to identify the sustainability topics that are material to the company. A central step in this process is determining company-specific IROs (Impacts, Risks & Opportunities) to derive the material sustainability topics. Both the potential financial effects of sustainability issues on the company and the company's impact on the environment and society are analyzed. A detailed overview of the Double Materiality Assessment and examples of IROs can be found here.

The European Sustainability Reporting Standards (ESRS) outline the specific requirements of the CSRD and define a total of 92 sustainability topics (AR 16) that must be assessed for materiality. This list is also referred to as the longlist. To determine relevant IROs, all sustainability topics are analyzed along the value chain, categorized in terms of timing, and assessed for their severity (i.e., scale, scope, and irreversibility) and likelihood of occurrence.

Incorporating all relevant stakeholder groups through representatives is particularly important for a realistic and comprehensive evaluation. Through structured analysis and stakeholder dialogue, companies establish a robust foundation for transparent and strategically aligned sustainability reporting.

Involvement of stakeholders in IRO assessment for CSRD

Through interviews, questionnaires, or workshops, stakeholders and their representatives discuss, analyze, and document various sustainability topics. Each topic is then examined to determine whether it involves positive or negative, actual or potential impacts, opportunities, or risks. In stakeholder discussions, it is crucial to focus on the most significant IROs without getting lost in details. The following questions can be helpful:

- What do you think are the most material risks, opportunities and impacts that we see with our suppliers?

- Which industries/regions/materials do you think have the greatest risks/impacts?

Sustainability aspects for which no IROs can be identified are excluded from the list. If entire topic areas are excluded, they must be justified for the auditor. This process refines the initial longlist into a shorter list of company-relevant topics and their corresponding IROs.

Determining IROs under ESRS using gross assessment

IROs must always be determined on the basis of a gross assessment. This means that IROs - whether positive or negative - must be identified and evaluated independently, without offsetting counteracting effects. Measures to mitigate negative impacts, such as decarbonization efforts to reduce greenhouse gas emissions, must not be independently listed as positive impacts. Instead, they should only be considered when assessing the severity of the negative impact on climate change. Specific measures to reduce damage are later captured in the ESRS data points. The same logic applies to opportunities and risks.

Principles of the gross approach to IROs within the CSRD

1. Different types of impact: Positive and negative influences of different types must not be offset against each other. This ensures that each impact is identified and assessed without distortion.

2. Temporal separation: Current negative impacts cannot be offset by potential future positive impacts. The same applies to current positive impacts and potential negative ones.

3. Own operations vs. value chain: Impacts from a company’s own operations must not be offset against impacts along the value chain (upstream or downstream).

Actual negative impacts within the gross approach to IROs

If an actual negative impact exists, truly implemented countermeasures to mitigate the negative impact can be considered when assessing severity. For example, in the case of greenhouse gas emissions as an actual negative impact on climate change, implemented decarbonization measures can gradually reduce the severity rating - for instance, from 5 to 4 over time - until emissions are minimal or eliminated. In the first year, however, most companies in the industrial sector should expect to start with a severity rating of 4 or 5.

Positive impacts within the gross assessment of IROs

Positive impacts or opportunities should only be listed as IROs if:

- the negative impact in the same impact area (if any) is already listed as an IRO

- the positive impact is net positive, meaning it outweighs or offsets negative impacts or risks in the same area

- the positive impact is more than business as usual (BAU), meaning it goes beyond what is standard for comparable companies. "Business as usual" (BAU) can be defined in different ways or by different benchmarks. At the legislative level, BAU means the company fulfills the minimum legal requirements. In terms of industry standards, it refers to alignment with average practices within the industry. If the country standard is used as a reference, the company adapts to regional standards and expectations. Any impact above or below BAU is defined as a positive or negative IRO.

Supplementing with net information

In addition to gross figures, companies may provide information in net terms, meaning data that has already been adjusted. However, this presentation must not obscure relevant information, and the reasons for any adjustments must be clearly explained. The goal is to provide a realistic and undistorted picture of impacts, risks, and opportunities without distortion from potential mitigation measures. This ensures transparency.

The importance of gross assessment to IROs in CSRD

The CSRD explicitly states that IROs should be determined and assessed on a gross basis rather than net (i.e., considering other IROs/measures). Ensure that measures taken to mitigate a risk or negative impact are not listed as positive impacts or opportunities.

According to ESRS 1 “Appendix B: Qualitative Characteristics of Information” QC 8, a gross approach promotes neutrality and requires careful evaluation. Potential impacts, risks, and opportunities must be assessed as they are, without considering existing management measures. The severity of a potential IRO must be assessed independently of mitigation measures. This consideration applies only to actual IROs.

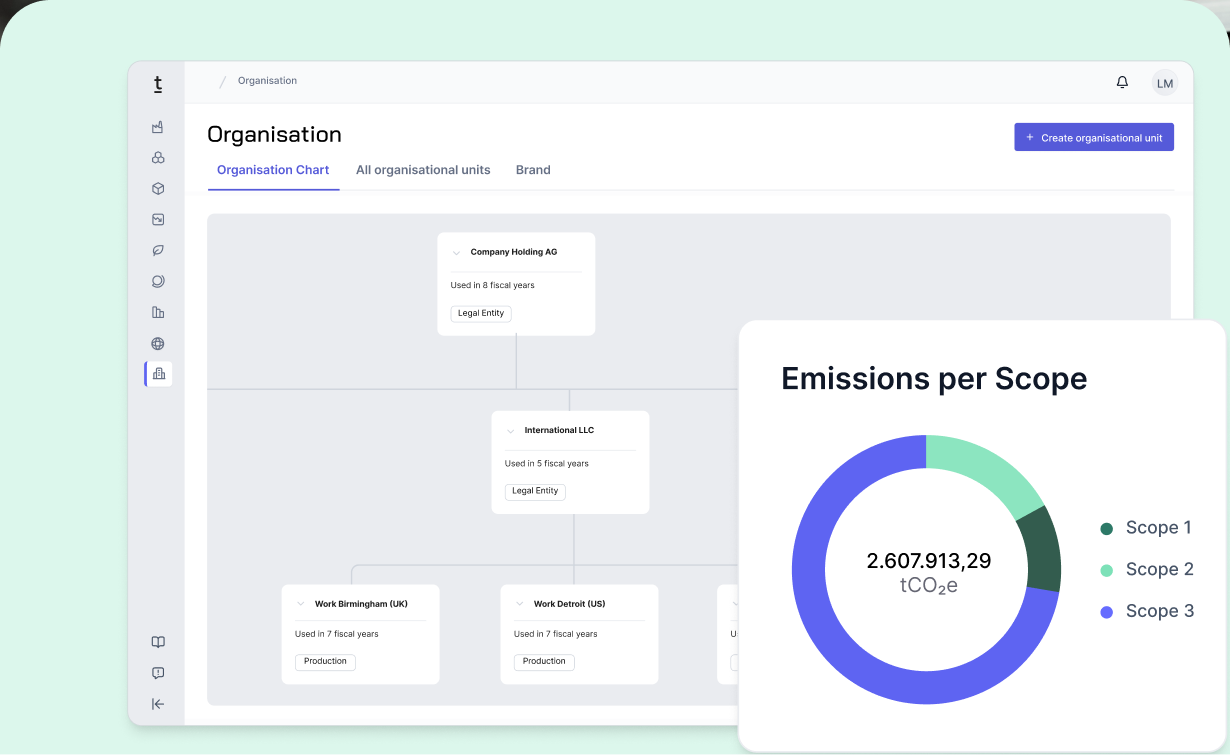

How does Tanso support you in assessing IROs according to ESRS?

When conducting the Double Materiality Assessment, Tanso software enables you to meet CSRD requirements and achieve sustainability goals through audit-compliant and integrated ESRS reporting at the highest standards. With our focus on data-intensive categories (e.g., Corporate Carbon Footprint), Tanso not only ensures standard-compliant reporting but also enables active management and optimization of ESG performance.

.avif)

.jpg)

.jpg)

-p-800.webp.avif)

-min-p-800.webp.avif)

-p-800.webp.avif)