Successfully Prepare for Double Materiality Assessment: Project Kickoff and Planning

The Corporate Sustainability Reporting Directive (CSRD) is a European directive that requires companies to publicly report on environmental, social, and governance (ESG) aspects and influences the European Accounting Directive. It modifies accounting regulations, mandating that certain companies produce a sustainability report in the future. Since the CSRD only broadly defines the content of these sustainability reports, the European Commission tasked the European Financial Advisory Group (EFRAG) with drafting a European sustainability reporting standard that clearly specifies the reporting obligations. The resulting European Sustainability Reporting Standards (ESRS) are to be used by companies when preparing their sustainability reports. The goal is to improve transparency and comparability in sustainability reporting, with particular emphasis on the principle of double materiality.

To effectively meet the requirements of the ESRS and CSRD, careful project planning is essential before conducting the Double Materiality Assessment (DMA). In this article, we examine the preparation for this assessment, provide an overview of the key steps in project planning, and clarify which stakeholders should be involved in the process.

The importance of Double Materiality Assessment for CSRD reporting

The double materiality assessment (DMA) is the first step in CSRD reporting and defines the reporting framework for affected companies. This analysis considers both the outside-in (financial materiality) and inside-out (impact materiality) perspectives, allowing companies to identify and report on their most significant sustainability issues. Through a double materiality assessment, companies can ensure that their non-financial reporting includes the relevant disclosure requirements, thus providing meaningful and stakeholder-oriented information.

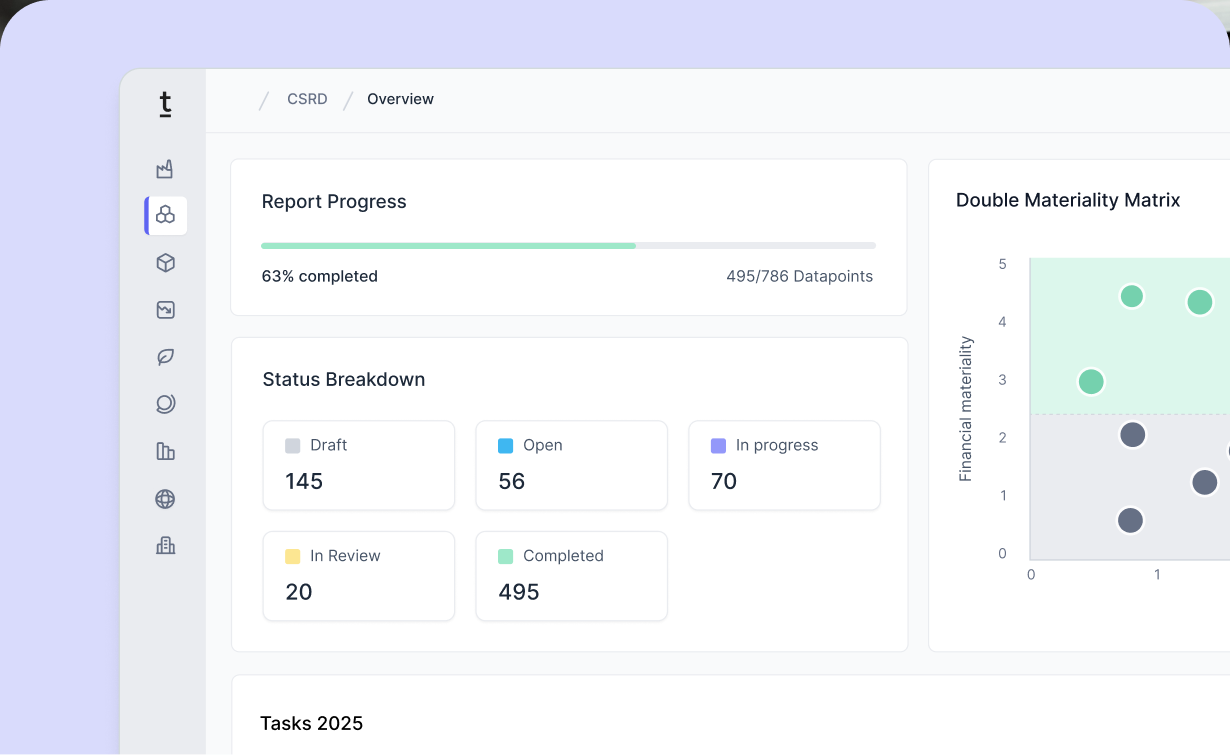

The disclosure requirements (DR) of the ESRS encompass around 1,200 data points in total, which must be reported depending on the results of the DMA. These data points cover general disclosures in ESRS 2 as well as the ten topic-specific standards, which are divided into Environmental, Social, and Governance (ESG) areas. While the scope of reporting for the topic-specific standards depends on the DMA, the general disclosures in ESRS 2 must be fully reported.

Preparing for the Double Materiality Assessment

Effective preparation for the double materiality assessment involves addressing key elements such as project team, timeline, and stakeholder engagement. Planning workshops and interviews is essential for identifying relevant topics, ensuring a balanced involvement of both internal and external stakeholders.

Project planning & framework

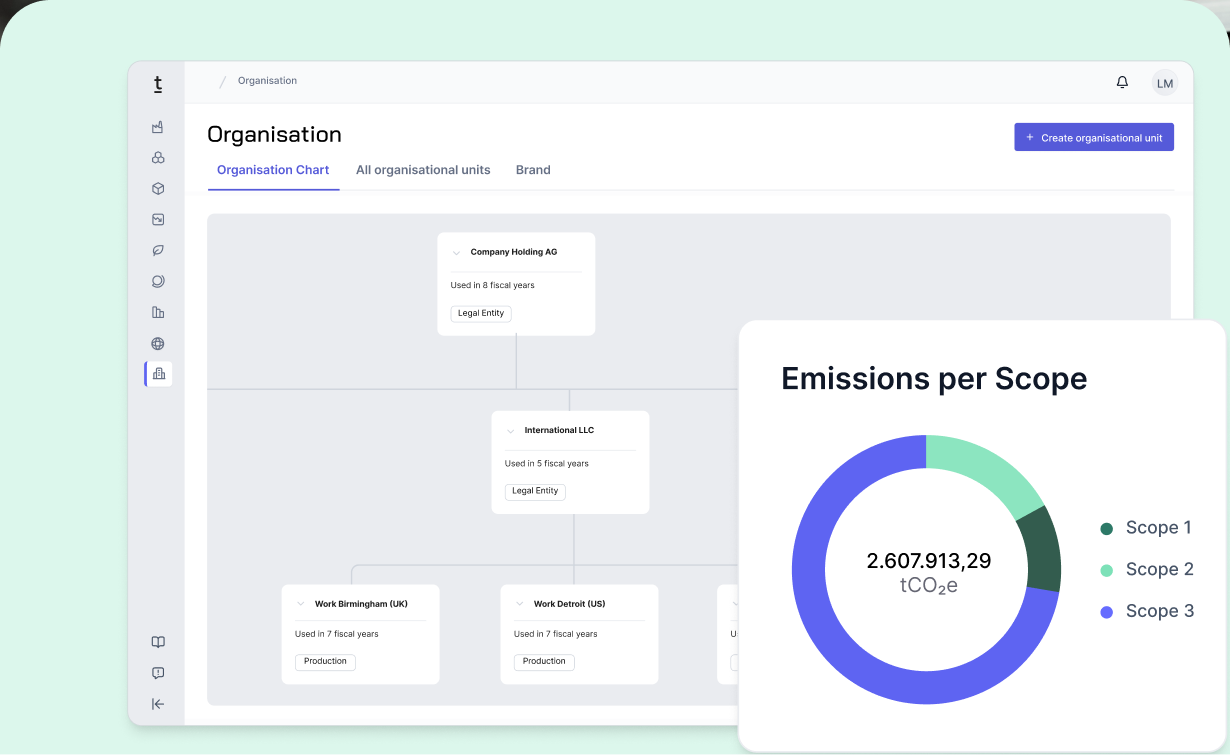

To tackle these questions, an internal project kick-off meeting can be highly beneficial. This allows for capturing management expectations and developing a thorough understanding of the organization’s business model and value chain. Key aspects to consider include the most revenue-driving sales regions, product segments, critical risks at production sites, and the workforce. This approach ensures a focused, company-specific execution of the double materiality assessment.

Drawing from experience and insights from expert networks and industry associations, we recommend leveraging the flexibility provided by the CSRD. Ambition levels may vary between auditors and are likely to rise after the initial reporting years. Therefore, engaging your auditor early and aligning on their expectations is a smart strategy.

Stakeholder involvement

When selecting stakeholders and engagement formats, it is advisable to strike a balance between the direct involvement of external perspectives and a pragmatic approach. Stakeholder involvement alone can take several months and tie up significant internal resources. External stakeholders can be replaced by internal representatives or experts, for example. Instead of a comprehensive employee survey, you can also convene a focus group of employees.

In addition, holding workshops with the respective stakeholder groups can be a more effective alternative to a company-wide survey. This is particularly true in view of the fact that internal stakeholder representatives can only make a useful contribution if they are “picked up” on the topic. If the stakeholder representatives do not develop an understanding of the topic, this leads to resistance and resentment among the company's own employees and delays the process immensely. In addition, the auditor may question whether stakeholder engagement has been properly implemented if the representatives, who are responsible for ensuring that the various perspectives of external stakeholders are included in the report, are unable to fulfill the task due to a lack of qualifications. It is therefore important that the procedure is documented in a comprehensible manner.

Affected stakeholders

Stakeholders with whom the company is connected through its products and services or its business relationships:

- Own workforce

- Workers in the value chain

- Affected communities

- Consumers and end-users

- Suppliers

- Nature as a silent stakeholder

Users of sustainability declarations

- Investors

- Lenders

- Insurances

- Business partner

- Trade unions

- Civil society and NGOs

- Regulatory bodies

Next steps after project planning: Conducting the Double Materiality Assessment (DMA) and integration into reporting requirements

Following the project planning phase, the next step is to conduct the Double Materiality Assessment (DMA), which aims to identify key sustainability topics and incorporate them into the relevant reporting requirements. A systematic and thorough data collection process is critical to ensure precise and meaningful sustainability reporting. Once the data collection is complete, the sustainability report must be audited by an external auditor to ensure compliance with legal requirements.

How Tanso supports your organization

With Tanso’s methodology for Double Materiality Assessment, developed in collaboration with auditors, you can significantly streamline the entire process and ensure a smooth, efficient analysis.

- Intuitive user guidance – Clear methodological guidelines make it ideal for anyone working with CSRD reports, regardless of experience level.

- Central data platform – Facilitates seamless collaboration with team members, consultants, and auditors for preparing and reviewing your DMA.

- Audit readiness – Ensures that all documentation requirements for audit preparation are covered within the audit process.

- Efficiency & automation – Automated pre-selection and assistance for over 100 ESRS data points, significantly reducing manual effort.

.avif)

.jpg)

.jpg)

-p-800.webp.avif)

-min-p-800.webp.avif)

-p-800.webp.avif)